GlobaPharm Pharmaceuticals

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

GlobaPharm, a $10B German pharmaceutical company specialising in small-molecule drugs, is considering acquiring BioFuture, a leading San Francisco-based biologicals start-up valued at $1B to rapidly enter the fast-growing biologicals segment. This case covers acquisition criteria, pipeline valuation methodology, break-even analysis on R&D investment, and post-merger integration risks.

- GlobaPharm has a long track record in small-molecule drugs (e.g., aspirin, blood pressure medications) but has no biologicals capabilities. - Biologicals are a rapidly growing drug class treating conditions beyond the reach of traditional drugs — competitors are already several years ahead. - BioFuture was founded 12 years ago by prominent scientists, employs 200 people, and is publicly traded at approximately $1B market capitalisation. - GlobaPharm's options for entering biologicals: build from scratch, partner with start-ups, or acquire. It has chosen to pursue acquisition. - McKinsey has been engaged to evaluate whether GlobaPharm should acquire BioFuture and advise on strategic fit.

Should GlobaPharm acquire BioFuture at its current $1B valuation, and does BioFuture's pipeline, capabilities, and strategic fit justify the investment, accounting for integration risks and the significant R&D investment required to unlock its full value?

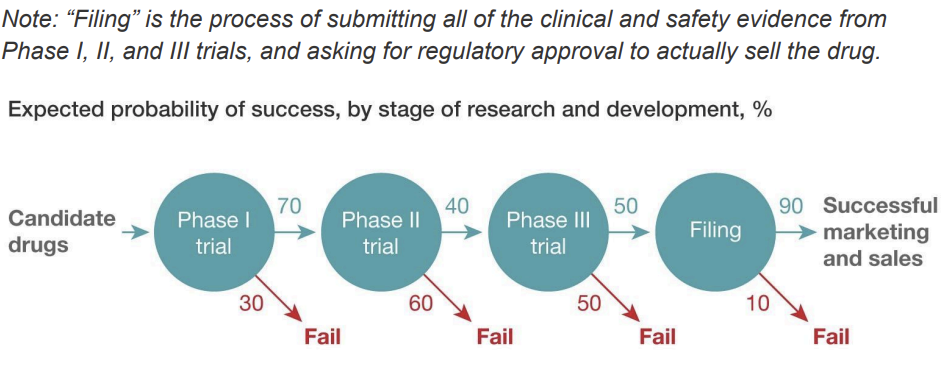

- Structure the acquisition evaluation across three axes: strategic fit, financial value, and integration risk - Conduct a drug pipeline DCF valuation adjusted for stage-specific success probabilities — do not rely solely on market capitalisation - Benchmark BioFuture against alternative acquisition targets and partnership options before committing to exclusivity - The 80% Phase II success rate threshold is a critical insight — present this to the board as a risk flag on additional R&D investment - Design a culture integration plan pre-close: ring-fence BioFuture's R&D team, preserve flat hierarchy and scientific autonomy - Retain key scientific founders through equity rollovers, milestone bonuses, and academic publication rights - Establish a joint scientific committee to align therapeutic focus and avoid duplicative R&D within 6 months of closing

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".