Diconsa

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

The Bill & Melinda Gates Foundation has engaged McKinsey to assess whether Mexico's government-owned Diconsa retail network - 22,000 stores serving rural communities - can be leveraged to deliver basic financial services to the rural poor. Currently, rural families travel long distances at significant cost and personal risk to collect government benefits from state bank branches. This case examines the feasibility, benefits, risks, and rollout strategy for using Diconsa as an agent banking network.

- The majority of Mexico's rural population is relatively poor and relies partly on government benefit payments for their livelihood. - Rural residents lack bank accounts and must travel to limited state-owned bank branches to collect cash benefits — a costly and risky process. - The Mexican government operates Diconsa: 22,000 stores supplying basic goods to rural populations, supported by central/regional warehouses and delivery trucks. - The Gates Foundation aims to extend basic financial services (benefits, savings, insurance, loans) to rural communities through the Diconsa infrastructure. - McKinsey has been asked to assess whether the Diconsa network can and should serve as an agent banking platform, starting with benefit disbursement.

Can Mexico's Diconsa store network feasibly and effectively serve as a platform for delivering basic financial services to rural populations, and what are the risks, benefits, and implementation challenges involved?

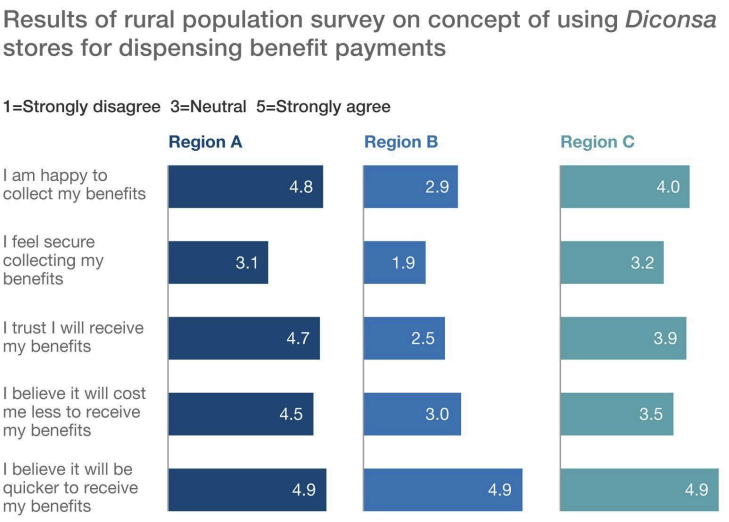

- Structure the assessment around three pillars: demand-side benefits, supply-side feasibility, and risk management - Quantify the consumer value proposition (450M pesos annual savings) as the headline case for rollout - Segment regions by receptivity and crime rate — start pilots in high-trust, lower-risk regions - Design a phased product roadmap: benefit disbursement first, then savings, insurance, and credit products as trust builds - Engage Diconsa store managers as financial agents with incentive structures tied to product take-up - Collaborate with state bank on fraud prevention infrastructure: chip cards, daily transaction limits, store-level reporting - Commission qualitative community research in Region B specifically before investing in rollout there

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".