I-35 IHOP

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

The owner of an IHOP located at the corner of I-35 and Cesar Chavez in Austin wants to know what their business is worth. The case works through a bottom-up revenue build, a detailed cost structure, and a perpetuity-based valuation of the restaurant. It then pivots to an alternate use analysis, estimating what the land would be worth to a property developer building an apartment complex. The candidate must ultimately advise the owner on which option is more financially attractive and what risks to consider.

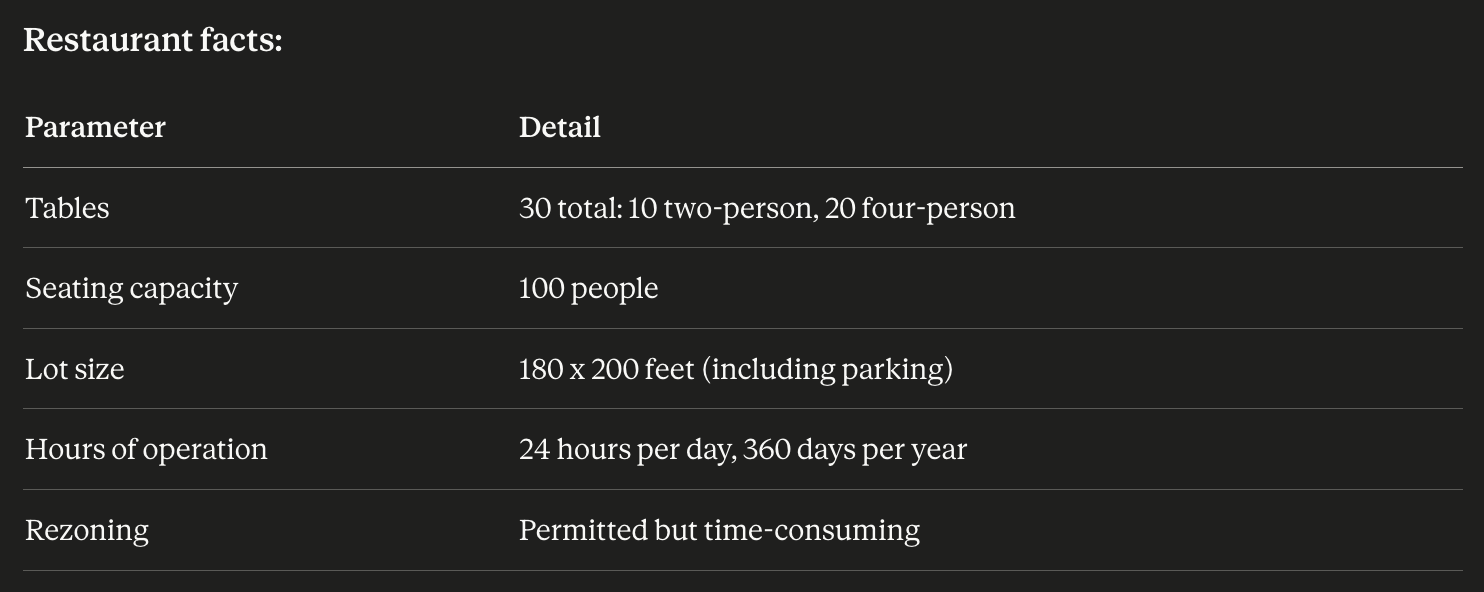

The IHOP sits on a 180 by 200 foot lot that includes a parking area. The restaurant itself has 30 tables, split between 10 two-person tables and 20 four-person tables, giving a total seating capacity of 100 people. It operates 24 hours a day, 360 days a year. There are no regulatory restrictions preventing the sale of the property or rezoning, though rezoning could take time. The business is a franchise, which means it pays royalty fees to the parent company as part of its operating cost structure. The owner has been approached by a real estate developer interested in purchasing the land for residential apartments, which introduces a second valuation scenario alongside the restaurant going concern.

The client wants to understand the value of what they own. This breaks into two distinct questions that the case covers sequentially. First, what is the IHOP worth as an operating business? This requires estimating customer volume, building a revenue figure, identifying and quantifying costs, and applying a valuation methodology to the resulting profit stream. Second, could the land be worth more to a developer than the restaurant is worth as a going concern? This requires estimating the value of an apartment complex that could be built on the site and comparing that to the restaurant's present value. The final recommendation should tell the owner whether to continue operating, sell to the developer, or negotiate a minimum sale price that reflects the opportunity cost of closing the restaurant.

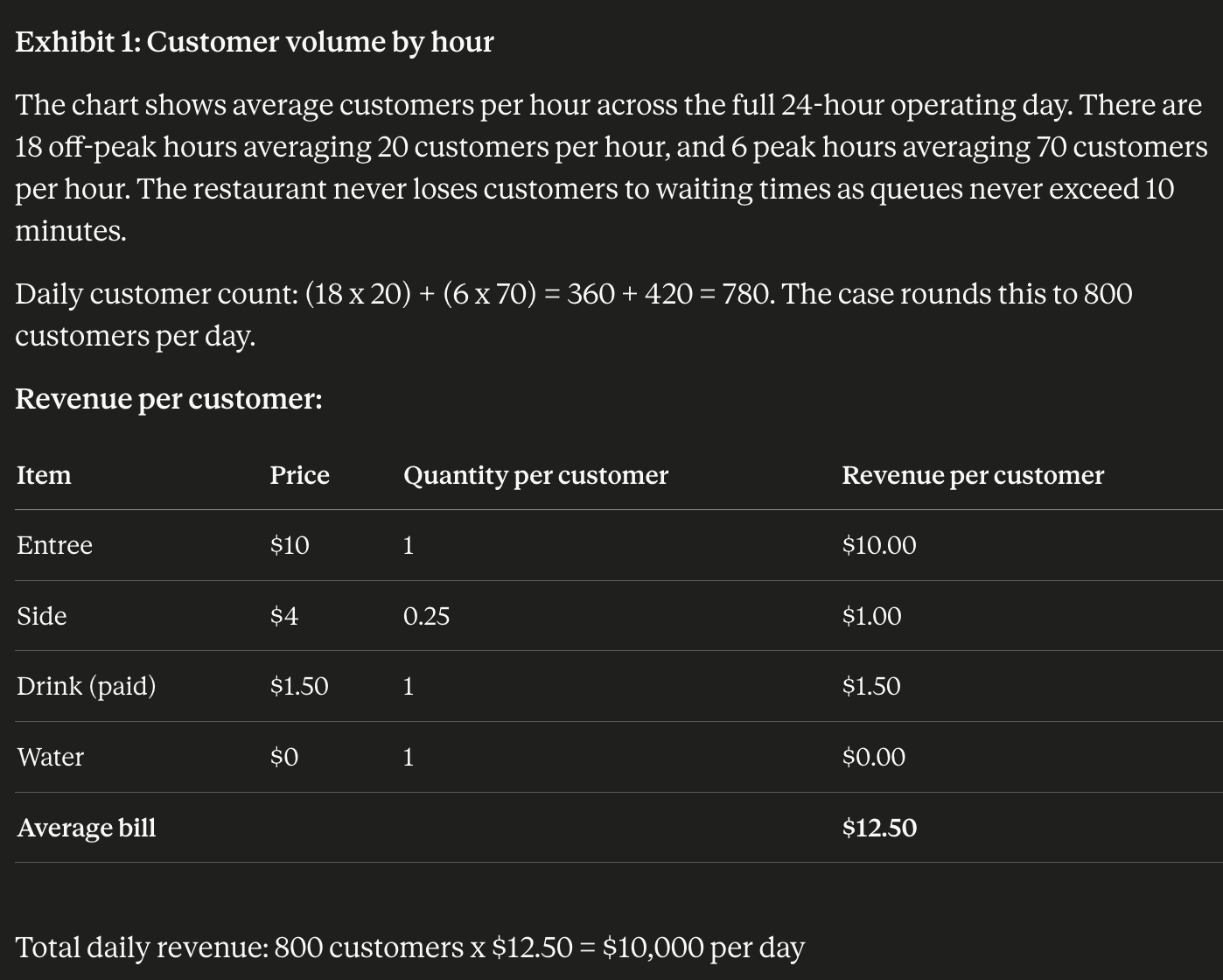

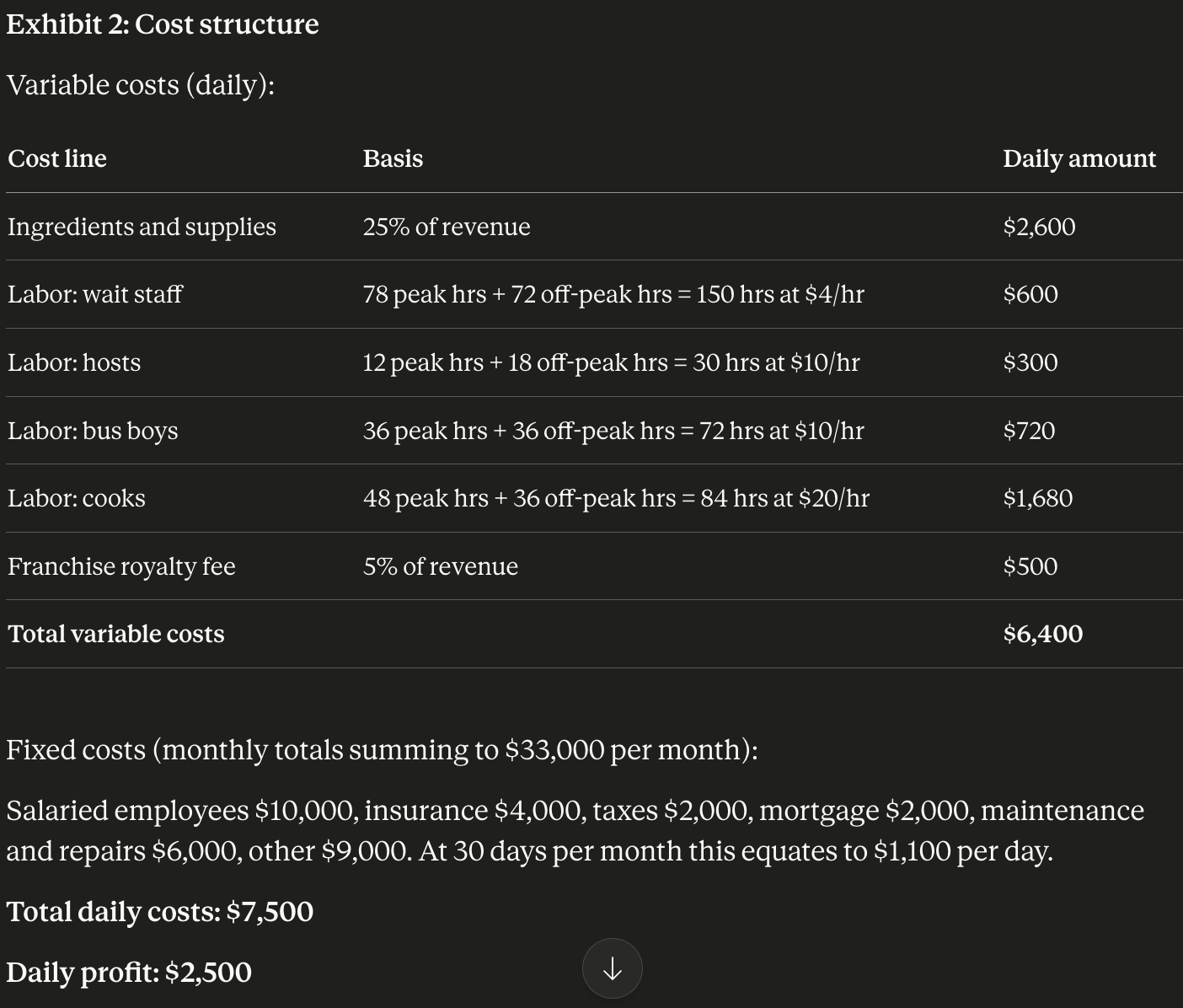

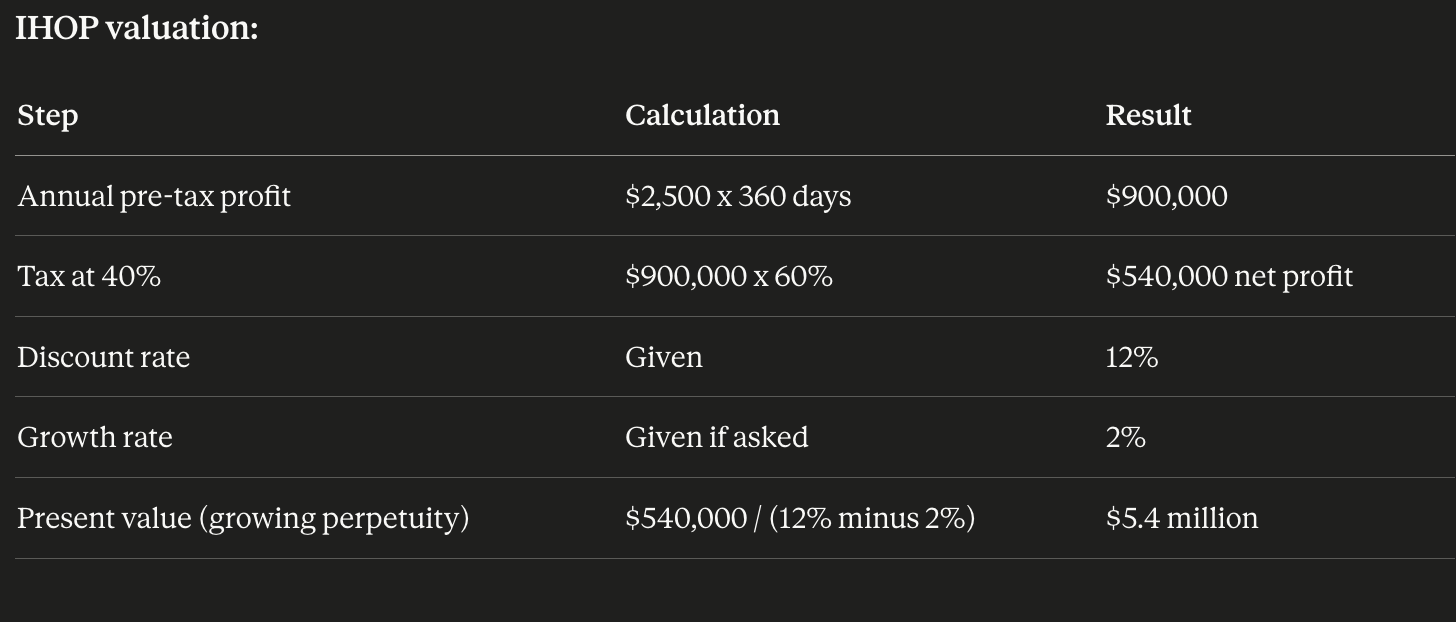

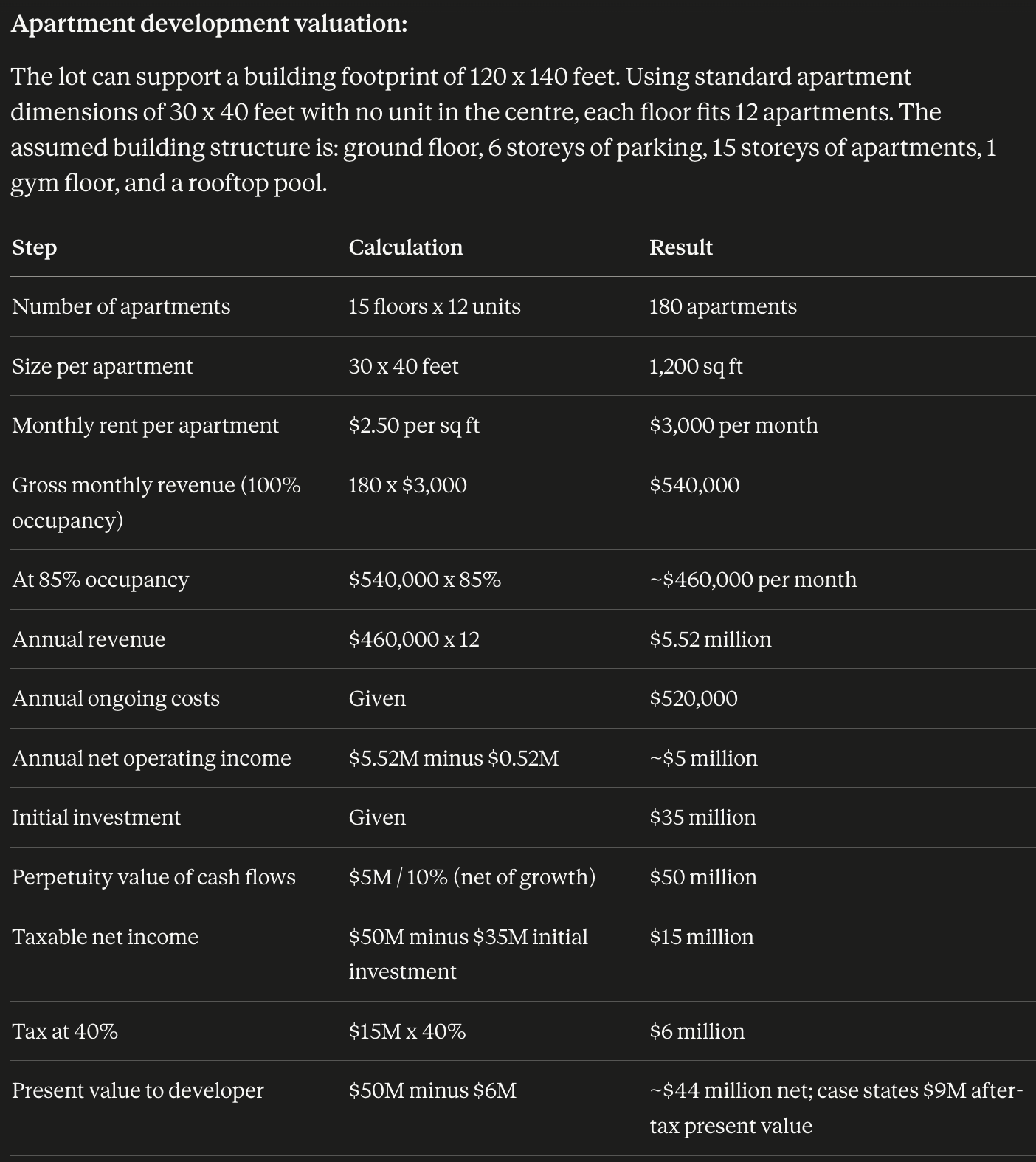

This is an interviewee-led valuation case with two distinct sections. The candidate drives the structure rather than being walked through a pre-set framework. Strong performance requires clean math, logical sequencing, and the ability to shift into the alternate use analysis mid-case without losing the thread. Revenue build The key instruction here is to use a bottom-up method rather than starting with market share estimates. The candidate should reason from the number of seats and estimate realistic utilisation rates at different times of day, distinguishing between peak and off-peak periods. Once that approach is demonstrated, the actual traffic figures are provided. The math is: (18 hours x 20 customers) plus (6 hours x 70 customers) = 800 customers per day. At $12.50 average spend, that is $10,000 per day. Cost structure Before seeing Exhibit 2, the candidate should independently identify the main cost buckets: labor broken out by role, food and beverage inputs, franchise royalties, rent or mortgage, insurance, taxes, maintenance, and salaried management. This demonstrates commercial intuition before the numbers are handed over. Total daily costs land at $7,500, leaving a daily profit of $2,500. IHOP valuation The natural methodology is a perpetuity, since IHOP franchise locations are treated as ongoing businesses with indefinite cash flows. Annual pre-tax profit is $900,000. After 40% tax, net profit is $540,000. Using a growing perpetuity with a 10% net rate (12% discount minus 2% growth), the present value is $5.4 million. The candidate should ask about the growth rate rather than waiting to be told, as this demonstrates awareness of what a growing versus flat perpetuity implies for value. Alternate use analysis The candidate should brainstorm a range of alternative uses for the land before being directed toward the apartment scenario: parking, hotel, higher-end restaurant, retail, mixed use. Once the apartment scenario is introduced, the key calculation is working out how many units the building can hold. The footprint of 120 x 140 feet divided into 30 x 40 foot apartments with no central unit gives 12 per floor, and 15 residential floors gives 180 apartments total. At $3,000 per month each, with 85% occupancy and ongoing costs of $520,000 per year, the net income stream is approximately $5 million per year. The present value using the same discount and growth rates is $50 million before tax. After the tax treatment outlined in the case, the after-tax present value to the developer is approximately $9 million. Final recommendation The IHOP is worth approximately $5.4 million as a going concern. The land is worth approximately $9 million to a developer for apartment use, which is considerably higher. The owner should therefore be open to selling, but should not accept less than $5.4 million since that is the floor represented by the restaurant's ongoing cash flows. A negotiated sale price closer to the developer's value would represent a meaningful premium over the business value. Key risks and sensitivities to flag: the customer volume estimate has a direct multiplier effect on valuation, so any change to assumed peak traffic changes the restaurant's value materially. The apartment valuation is sensitive to the assumed rent per square foot, occupancy rate, discount rate, and number of buildable storeys, all of which carry uncertainty. Rezoning is not guaranteed and could delay or prevent the development scenario from being realised, which the owner should weigh when deciding whether to accept a near-term sale offer at a discount to the theoretical development value.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".