Miller Brewing Company Merger

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

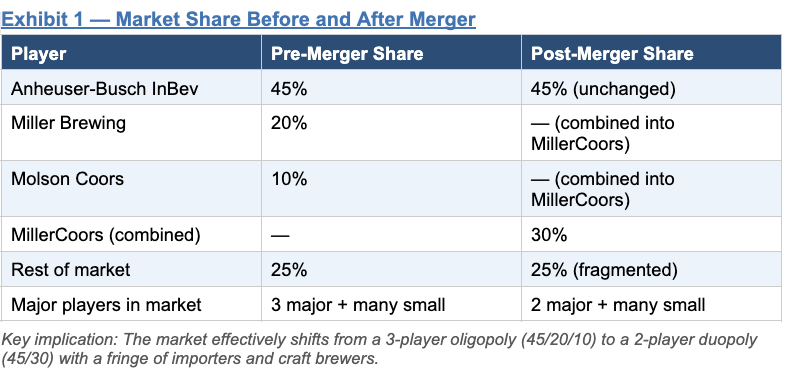

Miller Brewing Company (the #2 U.S. brewer, 20% market share) and Molson Coors (the #3 player, 10% market share) are merging to form MillerCoors, creating a combined entity with 30% of the U.S. beer market. The dominant player, Anheuser-Busch InBev (ABI), holds 45%. The candidate is asked to assess what will happen to the U.S. beer market post-merger and to identify and rank the key synergies available. This is a dual-lens case: part market structure analysis (oligopoly dynamics, competitive response) and part M&A synergy analysis (cost savings and revenue upside). Strong candidates will address both the quantitative synergy logic and the qualitative competitive implications — including the risk of tacit coordination and regulatory scrutiny.

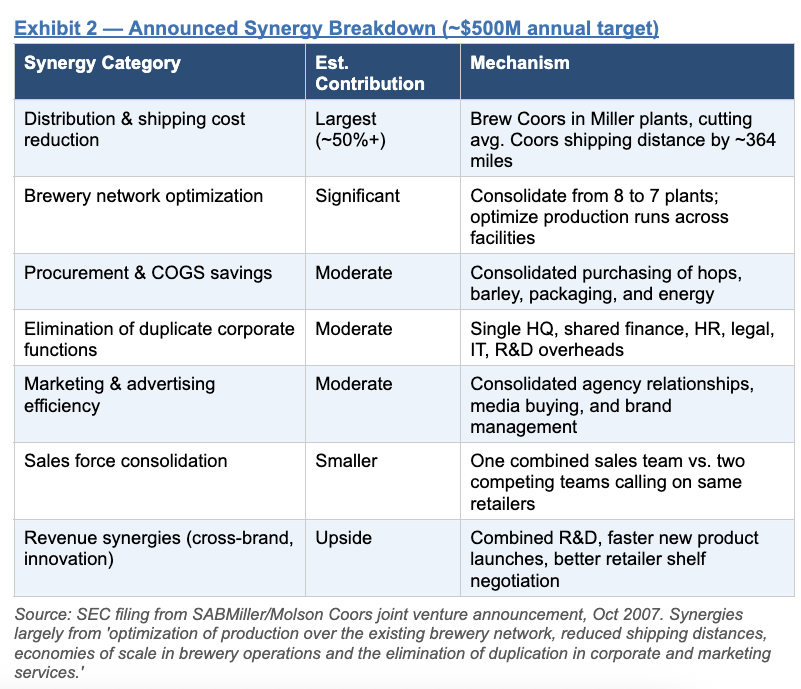

Client: Miller Brewing Company, Milwaukee, Wisconsin Counterpart: Molson Coors Brewing Company Transaction: Joint venture of US and Puerto Rico operations, announced October 2007, approved by DOJ June 2008, operations began July 1, 2008 Brewing Footprint (pre-merger): Miller: 6 brewing plants distributed across the U.S. Coors: 2 brewing plants (Golden, CO and Shenandoah, VA), much more geographically concentrated Combined entity: 8 plants, then consolidated to 7 — significantly reducing average shipping distance for Coors products (average reduction: ~364 miles to key markets) Transaction Structure: SABMiller (Miller's parent) received 58% economic interest; Molson Coors received 42% economic interest Both parties held equal 50/50 voting rights and equal board representation (5 seats each) Projected annual synergies at announcement: ~$500 million

What will happen to the U.S. beer market after the Miller–Molson Coors merger? What are the key synergies available to the combined entity, and how should they be prioritized? Two core questions to address: Market impact question: How does the merger reshape competitive dynamics in the U.S. beer market — for MillerCoors, for ABI, and for smaller players? Synergy question: What are the sources of cost and revenue synergy, how large are they, and which should be pursued first? Why this merger happened (strategic logic): Scale is critical in brewing — fixed costs are high (plants, distribution infrastructure, brand marketing), making larger volumes essential to cost competitiveness ABI's dominance at 45% gave it structural advantages in pricing, retailer shelf space, and distributor relationships that neither Miller (20%) nor Coors (10%) could match alone A combined 30% share creates a more credible #2 competitor with the scale to invest in marketing, distribution optimization, and innovation

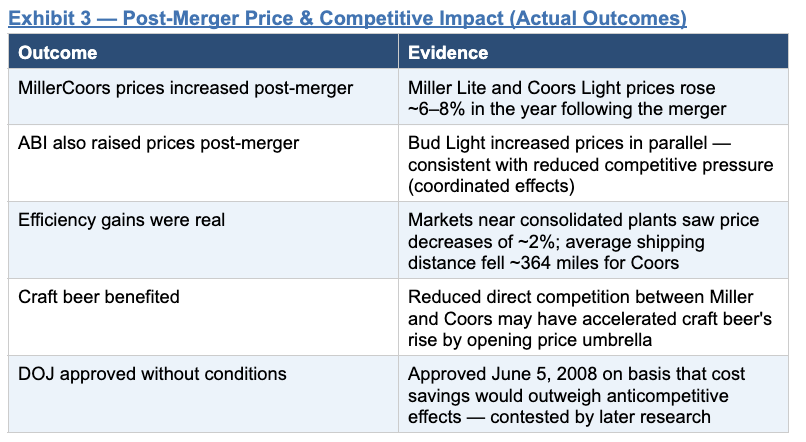

Framework: Answer Both Questions in Sequence This case has two distinct asks. Answer them in order: (1) market impact, then (2) synergy analysis. A strong candidate structures their response clearly before diving in. Step 1 — Analyze the Market Impact Start with the math: 20% + 10% = 30% combined, vs. ABI at 45%. The market goes from a three-player oligopoly to a two-player near-duopoly. Competitive dynamics shift: Miller and Coors were competing against each other as much as against ABI. Post-merger, all competitive energy is directed at ABI — making the #2 player more formidable. Pricing implications: With fewer independent competitors, the incentive to hold prices down through competition weakens. Historically, MillerCoors and ABI prices rose ~6–8% in the two years after the merger. ABI response: ABI may feel less pressure to compete aggressively on price, potentially benefiting from the "price umbrella" effect — a key concern for antitrust regulators and consumers. Impact on craft and imports: If the macro brewers tacitly align on premium pricing, craft brewers and imports (Corona, Heineken) gain room to grow share — which is partly what happened post-2008. Step 2 — Identify and Rank Synergies Cost Synergies (primary value driver — ~$500M targeted) Distribution / logistics (highest priority): Coors was brewed in only 2 locations vs. Miller's 6. By brewing Coors in Miller plants, the average distance to customers dropped ~364 miles, directly cutting shipping and fuel costs. This was the single largest identified synergy and the primary rationale accepted by the DOJ. Brewery network optimization: Consolidating from 8 to 7 plants eliminates excess fixed cost. Production scheduling across a shared network allows better utilization rates. Procurement / COGS: A combined buyer of hops, barley, cans, bottles, and refrigeration equipment commands better terms from suppliers. Beer ingredients and packaging are commodity markets where scale matters. Corporate overhead elimination: Two full corporate functions (finance, HR, legal, IT, C-suite) become one. This is a standard M&A synergy — elimination of duplication. Marketing / agency consolidation: Combined advertising spend gives more leverage with media buyers and reduces the cost of running two separate brand organizations. Revenue Synergies (secondary, harder to realize) Cross-distribution: Miller brands could be introduced into Coors' strong Western US markets; Coors brands could gain distribution in Miller's Midwest/East strongholds. Retail shelf negotiations: A combined portfolio with 30% market share gives the sales force more credibility and leverage in negotiations for shelf space and promotional placement. Innovation and new product launches: Shared R&D, faster time-to-market for new products, and the ability to test across a broader geographic footprint. Step 3 — Prioritize the Synergies Rank synergies by: (a) size of impact, (b) speed of realization, and (c) implementation risk. Final Recommendation The Miller–Molson Coors merger is strategically sound and financially compelling. The combined entity should: Prioritize distribution and logistics synergies first — they are the largest, fastest, and least risky to capture, and were the primary basis for DOJ approval Pursue overhead consolidation in parallel, targeting duplicate corporate functions before touching customer-facing roles Execute brewery optimization cautiously — the network benefits are real, but plant closures carry execution and reputational risk Monitor competitive dynamics closely — the risk of inadvertent (or deliberate) price coordination with ABI is real and was documented post-merger; MillerCoors should maintain independent pricing discipline to avoid antitrust exposure Invest aggressively in brand differentiation for the combined portfolio — in a two-player market, brand equity becomes the primary competitive battleground as price competition softens Candidate Tips (Interviewer Notes): Structure matters enormously here — lay out that you will answer market impact first, then synergies, before diving into either The key market insight is the shift from a 3-player oligopoly to a 2-player near-duopoly, and what that means for pricing incentives For synergies, the interviewer wants to see a ranked list with logic — not just a brainstormed inventory. Distribution is clearly #1 given the brewery geography. Strong candidates will raise the antitrust angle and tacit coordination risk — it shows real business awareness and awareness of the actual case outcome Be ready for: 'What would you advise ABI to do in response?' — a strong answer involves ABI accelerating its own cost reduction and perhaps looking at its own M&A (InBev acquisition of AB happened the same year, 2008)

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".