Phighting Phillies

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

Our client, Alpha Capital, is a private equity firm that is considering buying the Philadelphia Phillies. The current team owners approached Alpha about purchasing the team for $1.1B. Alpha engaged our firm in the due diligence process and wants us to help them understand whether to buy the team.

Alpha Capital is a private equity firm evaluating the acquisition of the Philadelphia Phillies MLB franchise. The current owners have approached Alpha with an asking price of $1.1 billion. Alpha has engaged consultants to support the due diligence process. This is a new standalone fund with no hold period constraints, no prior investments, and hurdle rates are not a binding constraint. The motivation is dual: maximize financial returns, and the fund's leadership are avid Phillies fans who want the team to win. The team does not own its stadium; the City of Philadelphia owns it and the team pays annual leasing costs. Spring training and the farm system are excluded from the analysis. The case has two core deliverables: arrive at a standalone valuation of the team, then assess whether the acquisition makes sense after accounting for synergies and qualitative considerations.

(read to candidate): Our client, Alpha Capital, is a private equity firm that is considering buying the Philadelphia Phillies. The current team owners approached Alpha about purchasing the team for $1.1 billion. Alpha has engaged our firm in the due diligence process and wants us to help them understand: A. What is the team worth? B. Should they make this investment? The two-part decision: Part A - Valuation: Build a revenue and cost model from first principles, then apply a discount rate to arrive at an intrinsic value. Part B - Investment Decision: Compare valuation to asking price, identify synergies that could bridge any gap, and assess qualitative risks before making a final recommendation. Interviewer note: Before revealing revenue and cost figures, ask the candidate to brainstorm revenue streams and cost drivers from scratch. This brainstorm is scored separately from the math.

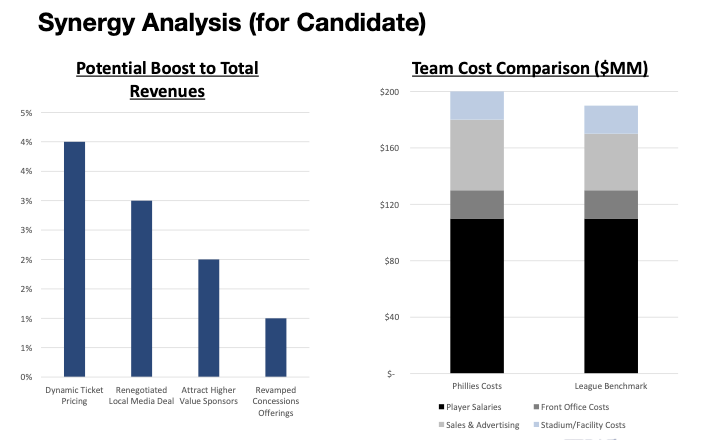

Framework This is a classic M&A/PE due diligence case with two sequential analyses. The candidate must first build a valuation from first principles - not apply a generic framework and then stress-test it with synergies and qualitative risks. Brainstorm Revenue & Costs → Build P&L → Arrive at Standalone Valuation → Compare to Asking Price → Identify Synergies → Revised Valuation → Qualitative Considerations → Recommendation The pivotal realization is that the deal only works with synergies. A candidate who stops at the standalone valuation and says "don't buy" misses the point entirely. A candidate who breezes past the gap without identifying synergies has the same problem. Standalone Valuation vs. Asking Price The standalone valuation of $1.0B falls $100M short of the $1.1B ask. This should prompt the candidate to hunt for upside and not walk away. Synergy-Adjusted Recommendation Recommendation: Alpha should proceed with the acquisition at $1.1B - conditional on execution of synergies. Three reasons: The deal is accretive with synergies. At a synergy-adjusted valuation of $1.4B, Alpha acquires the team at a $300M discount to intrinsic value. The $40M in annual synergies is well-supported by benchmarking data. The largest synergy (Sales & Advertising) is highly credible. The $10M cost gap vs. the league benchmark is specific and actionable - a PE firm with operational expertise is exactly the right buyer to close it. Revenue initiatives are realistic. Dynamic ticket pricing (already standard in other sports) alone contributes $12M annually. Combined with a renegotiated local media deal and a more structured sponsorship approach, the 10% total revenue uplift is achievable within 2–3 years. Risks to Flag Execution risk: Synergies are not guaranteed. If only 50% are captured, the valuation premium shrinks to ~$200M is still positive but with less cushion. Tension between ROI and winning: Cutting player salaries to maximize profit could alienate fans and erode the very revenue streams the model depends on. League approval and fan reaction: MLB controls who can own franchises; PE ownership is scrutinized. Fanbase trust must be managed carefully to protect ticket and sponsorship revenues. Macro baseball risk: Declining youth participation and cord-cutting trends could pressure media rights to the single largest revenue line at $120M.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".