BankCo

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

Our client is BankCoCard, a US credit card subsidiary of the major international bank BankCo. They have a rapidly growing $16 billion dollar credit card portfolio. BankCoCard is interested in lowering their cost of funds for their credit card program by starting an online bank.

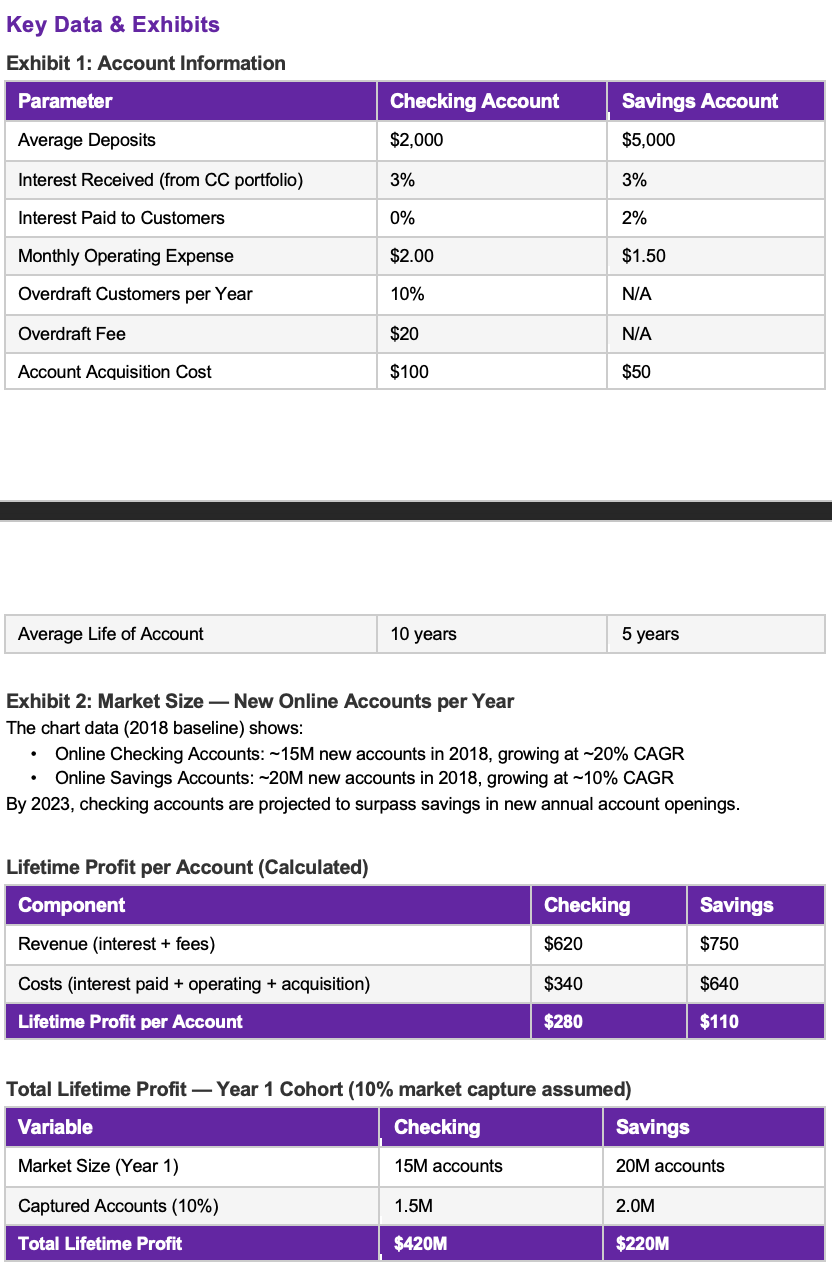

BankCoCard is a US credit card subsidiary of BankCo, a major international bank. The company manages a rapidly growing $16 billion credit card portfolio. Its current cost of funds stands at 4%, which management seeks to reduce by launching an online bank that would use customer deposits to fund the credit card portfolio at a 3% internal interest rate. BankCoCard wants to launch both a savings and a checking account, but its IT budget only allows one product to be built this year. The unchosen product would be launched the following year. Both products are expected to take the same time and cost the same amount to build ($10 million each). Interest rates are not expected to change for the foreseeable future.

Should BankCoCard launch an online bank? If yes, should it launch a savings account or a checking account first to maximize lifetime profitability while also addressing the objective of lowering cost of funds for its credit card portfolio?

Structured Approach • Step 1 – Compute lifetime profit per account: For each product, calculate revenue over the account lifetime and subtract all associated costs including acquisition. • Step 2 – Size the total opportunity: Apply 10% market capture rate to each market's annual new account openings to estimate the Year 1 cohort. • Step 3 – Assess strategic alignment: Consider the original objective — lowering the cost of funds — by estimating total deposits generated by each product. • Step 4 – Question suspicious assumptions: 10% market capture in Year 1 is aggressive. Consider sensitivity to lower capture rates. Key Insight The checking account generates nearly twice the lifetime profit per account ($280 vs. $110) and in aggregate ($420M vs. $220M). However, the savings account deposits are much larger ($5,000 per account vs. $2,000), meaning the savings product generates more deposit capital ($10B vs. $3B) — more directly addressing the stated goal of lowering cost of funds. An excellent candidate will surface this tension. Recommendation • Launch the checking account in Year 1 for superior lifetime profitability. • Follow with savings account in Year 2. • Acknowledge the strategic nuance: if cost-of-funds reduction is the primary goal, savings may deserve earlier prioritization. Key Risks • Capturing 10% of the market in Year 1 is aggressive and may overstate projected profits. • Product may not be sufficiently differentiated from competitors. • Regulatory requirements for online banking could delay or complicate launch. • Reputation risk if the product underperforms.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".