Mining

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

Our client is an Australian mining company, whose main product is Iron Ore, which it sells exclusively to China. This company is the largest producer in volume in this market with 230 million tons sold each year.

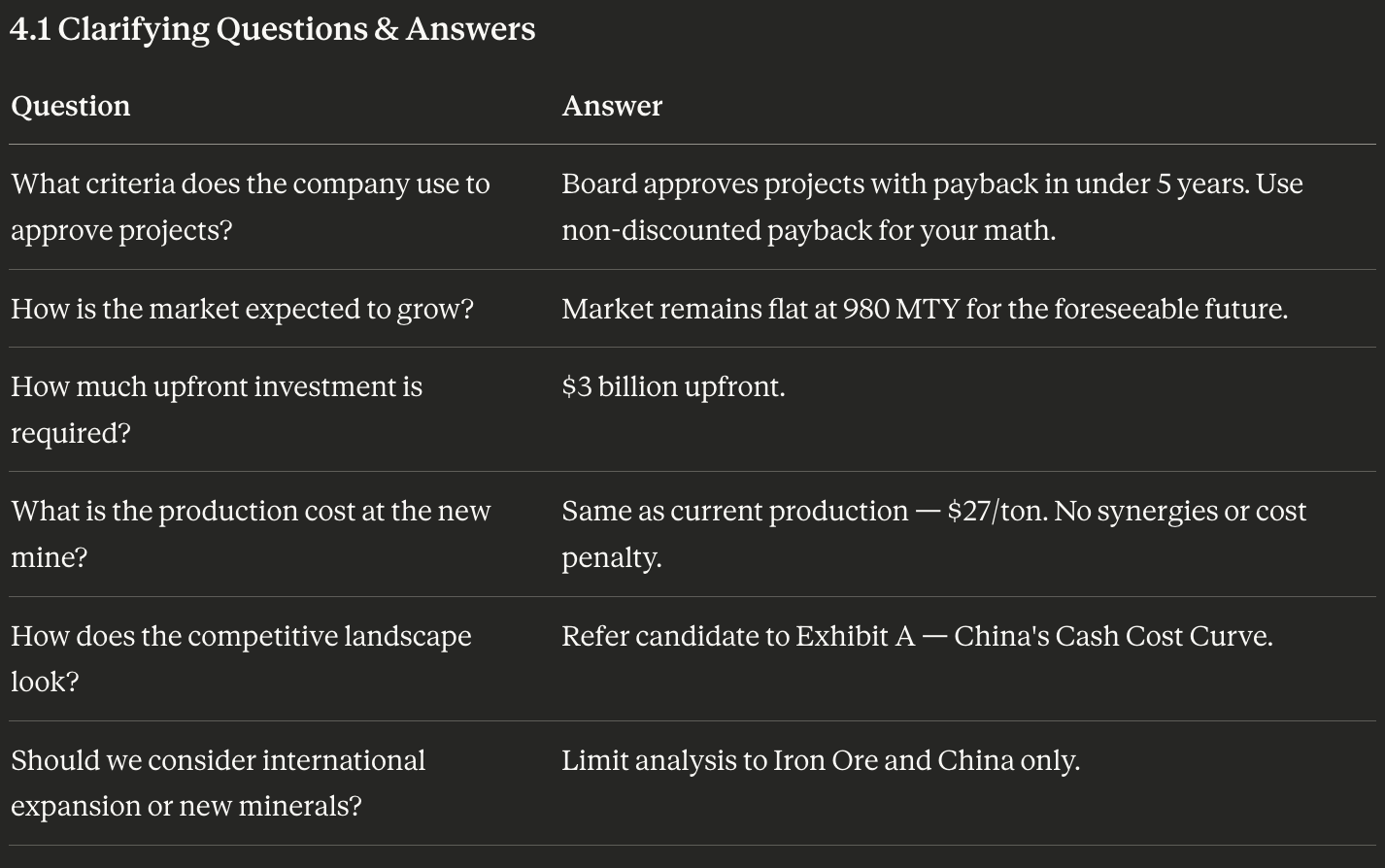

Our client is an Australian mining company that produces Iron Ore exclusively for the Chinese market. It holds two structural advantages: it is the largest producer by volume (230 million tons/year) and the lowest cost producer at $27/ton. Total Chinese demand for Iron Ore is approximately 980 million tons per year (MTY) and is expected to remain flat. The client has secured a concession to mine a new site adjacent to its largest existing operation. If developed, this would expand production from 230 MTY to 360 MTY — an addition of 130 million tons per year. The project requires a $3 billion upfront investment. Because Iron Ore is a commodity sold into a perfectly competitive market, any increase in supply by the client will affect the market-clearing price — making this a classic volume vs. price trade-off decision with significant competitive strategy dimensions.

(read to candidate): Our client is an Australian mining company whose main product is Iron Ore, which it sells exclusively to China. This company is the largest producer in volume in this market with 230 million tons sold each year. It is also the lowest cost producer at $27/ton. We estimate total Chinese demand for Iron Ore to be around 980 million tons per year. Our client has won a concession to mine a new site adjacent to its biggest mine and can increase production to 360 million tons per year and130 million additional tons. Is this worth doing? Core decision: Should the client invest $3B to expand production by 130 MTY, given that the expansion will depress the market price for Iron Ore?

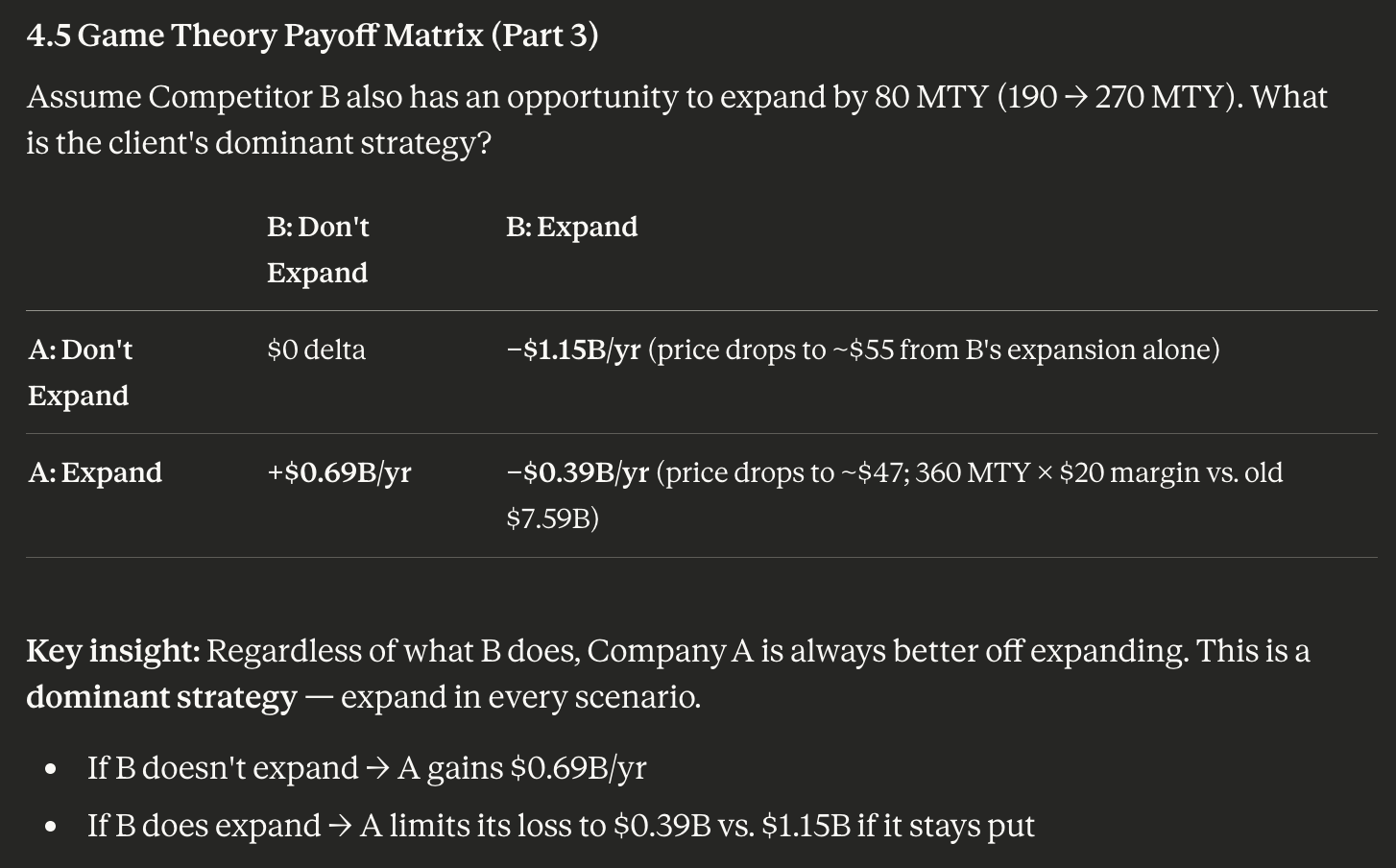

Framework This is a capital investment + competitive strategy case. A strong candidate builds a profit tree (Revenue = Price × Volume; Profit = Revenue − Costs) and recognizes immediately that the key tension is price compression from increased supply vs. volume uplift. The answer lives in the math, but the insight comes from the game theory. Profit Tree → Price Impact (via Cost Curve) → Payback → Competitor Reaction → Dominant Strategy Final Recommendation Recommendation: The client should expand — unambiguously. Three reasons: 1. Economics clear the hurdle. The expansion generates ~$690M/year in incremental profit, paying back the $3B investment in approximately 4 years — within the board's 5-year threshold. 2. Scale compounds the competitive advantage. As the lowest-cost producer at 360 MTY, the client can absorb the price drop better than any competitor. Higher-cost players are squeezed out entirely; Competitor B loses $1.9B/year in margin. 3. Game theory confirms it's a dominant strategy. Whether or not Competitor B expands, the client is always better off expanding — either capturing $690M/year in upside or limiting a downside loss from $1.15B to $390M. Risks to Monitor: - A sharp decline in Chinese steel demand could push the equilibrium price below the $27/ton cost floor for smaller producers and restructure the entire market - New mine discoveries or M&A among competitors could shift the supply curve left - Logistics constraints (port capacity, shipping) could limit the client's ability to deliver 360 MTY at the assumed cost

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".