TV Screens

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

This case involves Vivid, a consumer electronics manufacturer that produces high-definition TV (HDTV) screens. Despite increasing sales volumes, the company’s revenue has remained flat. The core of the case involves analyzing a complex supply chain, identifying misaligned sales incentives that lead to excessive discounting, and recognizing that Vivid’s high product quality and high customer switching costs provide significant untapped pricing power.

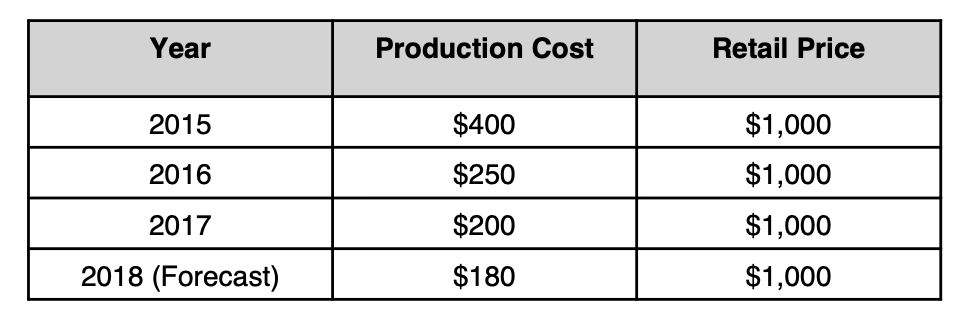

- The Client: Vivid, a manufacturer of patented HDTV screens. - The Customers: Major TV manufacturers in Asia and the US who integrate Vivid's screens into finished TVs for global retail. - Current State: Vivid's technology is patent-protected, and customers face high switching costs because switching would require expensive plant reconfigurations. - The Conflict: While production costs have dropped significantly due to economies of scale (from $400 in 2015 to a forecasted $180 in 2018), revenue is not growing

Vivid has retained SKP to perform a pricing optimization project. The company needs to determine why revenue is flat despite volume growth and how to better capture the value (surplus) it creates within the HDTV supply chain

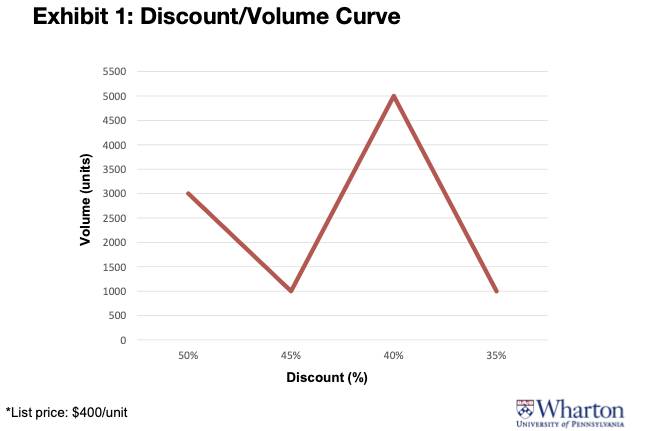

• Incentive Realignment: Shift sales compensation from volume-based quotas to profit-based metrics to reduce unnecessary discounting. • Discount Governance: Implement a stricter, multi-level approval process for discounts exceeding the standard floor. • Price Adjustment: Target an ASP of $240. This splits the $100 manufacturer/Vivid surplus more equitably ($40 for Vivid), giving both players a 20% return on sales.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".