Gold Mine

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

MyBank, a major financial institution managing a portfolio with 10% annual returns, has the opportunity to purchase an untapped gold mine in Peru from the Peruvian government for $250M. You must determine whether this investment deserves a place in MyBank's portfolio.

Client: MyBank Industry: Financial Services / Commodities Investment Geography: Peru (mine operations); Global (gold markets) Portfolio Benchmark: 10% annual return The Peruvian government seized a mineral-rich gold mine a decade ago and now wants to sell it to raise cash. The mine has not been developed since seizure. MyBank must evaluate whether acquiring it creates value beyond the 10% benchmark.

Assess whether the Peruvian gold mine is a sound investment for MyBank's portfolio relative to its 10% annual return benchmark, and identify conditions and risks that could affect the investment thesis.

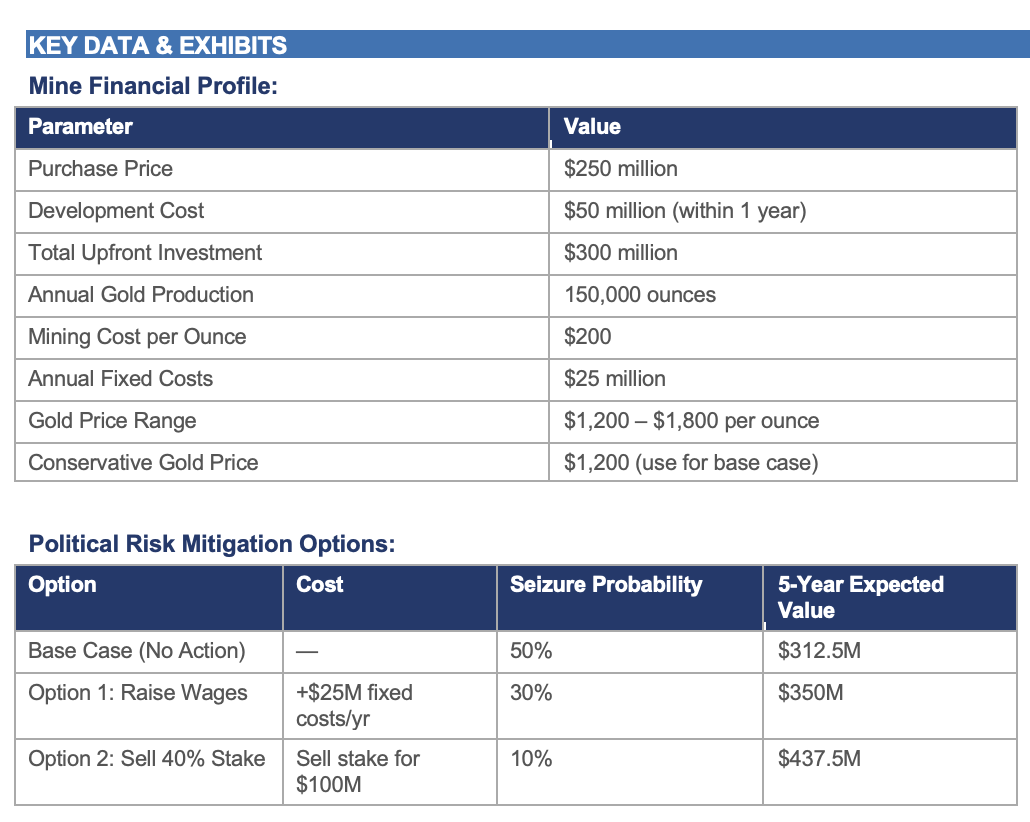

Q1 – Investment Worthiness Framework Assess across three dimensions: • Financial: Must exceed 10% annual ROI. Analyze setup costs, variable mining costs, gold production volumes, market price, mine longevity • Market: Gold market dynamics, price volatility, portfolio fit, alternative investment opportunities • Logistical: Mine operations (outsourced or in-house?), export infrastructure, labor pipeline, ethical considerations Q2 – Financial Analysis Using conservative gold price of $1,200/oz: • Margin per ounce: $1,200 − $200 = $1,000 • Annual gross profit: 150,000 oz × $1,000 = $150M • Annual net profit (after fixed costs): $150M − $25M = $125M • Payback period: $300M ÷ $125M ≈ 2.4 years (full return by year 3 of operations / year 4 overall) • 5-year total profit: $125M × 5 = $625M vs. $300M invested — well above the $450–480M at 10% annual returns Conclusion: This investment significantly outperforms the portfolio benchmark, even at conservative gold prices. Q3 – Key Risks • Political/Regulatory Risk: Peru seized this mine before — could do so again; export policy uncertainty • Gold Price Risk: A 50% drop in gold prices would eliminate profitability at current cost structure • Brand Risk: Is MyBank exploiting a cash-strapped government in a way that invites reputational harm? • Natural Disaster: El Niño or geological risk could disrupt or destroy operations • Labor: Local qualified workforce availability; wage expectations; talent pipeline sustainability • Infrastructure: Ability to transport gold from Peru to export markets Q4 – Political Risk Mitigation: Expected Value Analysis Three years in, a newly elected Peruvian president creates 50% seizure risk. Two mitigation options over a 5-year horizon (assumes $0 profit after seizure): • Base Case: ($125M × 5) × 0.5 = $312.5M expected value • Option 1 – Raise wages by $25M/yr: 5 × ($125M − $25M) × 0.7 = $350M — higher than base case • Option 2 – Sell 40% stake for $100M: (5 × $125M × 0.6) × 0.9 + $100M = $437.5M — highest expected value Recommendation: Option 2 (local partnership) dominates on a 5-year horizon. However, qualitative factors matter: • Long-term: Selling 40% permanently reduces ownership — does this make sense beyond 5 years? • Ethics: Does the $100M stake sale amount to a bribe to local interests? • Other options: Full liquidation (~$500M), direct government negotiations, or hybrid approaches

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".