Giant Bank

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

Giant Bank, one of the largest retail and commercial banks in the United States, is facing margin compression from rising operating costs and increased regulatory compliance requirements. Bain has been engaged to identify $200 million in sustainable annual cost savings without compromising customer experience or regulatory standing.

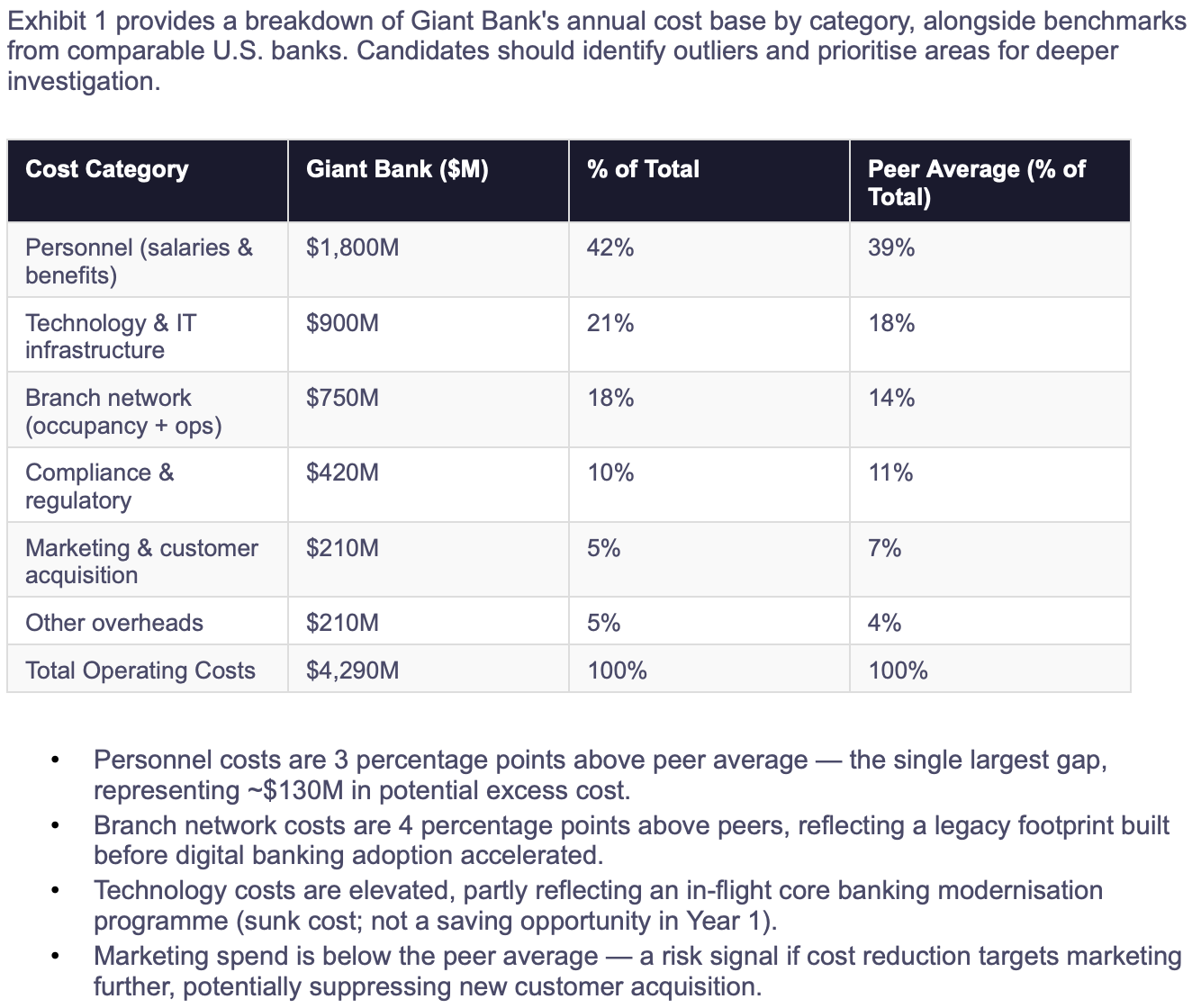

Giant Bank operates across four business lines: Retail Banking (45% of revenue), Commercial Banking (30%), Wealth Management (15%), and Investment Banking (10%). The bank has approximately 80,000 employees and 3,500 branches across the United States. Over the past three years, the bank's cost-to-income ratio has risen from 58% to 67%, driven by technology investment, compliance costs, and a wage-inflation cycle. The CEO has committed to investors that the ratio will be returned to 60% within two years. The engagement objective is to identify $200M in annual savings that can be achieved without headcount reductions that trigger regulatory or reputational risk. - Cost-to-income ratio deteriorated from 58% to 67% over 3 years - Target: $200M in annual savings; return cost-to-income to ~60% - 80,000 employees across 3,500 branches - Four business lines: Retail, Commercial, Wealth, Investment Banking - Constraint: no large-scale redundancies that generate regulatory/reputational risk

Bain must identify $200 million in sustainable annual cost savings across Giant Bank's operations. The analysis must distinguish between one-time cost reductions (e.g., asset disposals) and recurring savings, and must assess the feasibility, timeline, and risks of each lever. Key questions include: - Which cost categories represent the greatest opportunity for sustainable reduction? - What role can technology and automation play in reducing the cost base? - How should savings be allocated across the four business lines? - What is the risk of cost reduction initiatives adversely impacting customer satisfaction or regulatory compliance? - What sequencing and governance model should govern the cost programme?

A structured cost reduction engagement at a large bank requires a clear taxonomy of savings levers, rigorous prioritisation by impact and feasibility, and a sequenced implementation plan. The recommended approach: Step 1: Map the cost base — categorise all costs into fixed vs. variable, direct vs. overhead, and discretionary vs. non-discretionary to identify where flexibility exists. Step 2: Benchmark against peers — the data already reveals two high-priority areas: personnel (3pp gap) and branch network (4pp gap). Quantify the addressable gap for each. Step 3: Generate savings hypotheses — for each category, identify specific levers: branch consolidation, shared-service centres, vendor renegotiation, process automation, policy tightening on travel/entertainment. Step 4: Size and risk-rate each lever — assign a savings range (optimistic / base / conservative), implementation cost, timeline, and risk rating to build a prioritised opportunity map. Step 5: Design the programme — select levers that collectively deliver $200M p.a., sequence them by feasibility, and establish governance (programme management office, KPIs, executive sponsor). Step 6: Pressure-test for customer and regulatory impact — for each major lever, model the potential impact on NPS, attrition rates, and regulatory standing before committing. A strong recommendation would identify branch network rationalisation ($60–80M opportunity from reducing 350–400 low-footfall branches), workforce redeployment through shared service centres ($50–70M), and process automation in back-office functions ($40–50M) as the three primary levers, with a phased 24-month delivery timeline.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".