Brazilian Highway Concessions

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

A leading Brazilian highway concessions company wants to expand internationally to offset stalling domestic growth and reduce its concentration in the Brazilian economy. The case works through a market entry framework, a graphical analysis of South American markets, and a quantitative comparison of two entry routes: primary investment versus acquisition. The candidate needs to identify the right markets to target, choose a sensible entry mode, and back that recommendation with ROIC calculations.

The client is a leading Brazilian company that builds and operates public roadways under concession contracts. It operates solely in Brazil and its staff speaks primarily Portuguese. It wins business by bidding through competitive RFPs with municipal, state, and national governments as customers. There are no adjacent industries it is considering — road concessions are its only focus. Brazil's economic growth has stalled, and the client needs to grow both revenues and profits. International expansion is the chosen path. The company has already scoped some opportunities in South America and has a preference for that region, though it is open to considering all geographies.

The client faces three sequential decisions: Where to expand: Which international markets offer the best combination of business environment quality and pipeline of future projects? And should the search be limited to South America, or should the company look further afield? How to enter: Once target markets are identified, what is the right mode of entry — greenfield primary investment, a joint venture, or an acquisition? Which specific opportunity to pursue: Given that JV options have been ruled out, how do the primary investment and M&A routes compare on a financial basis, and which one should the client recommend?

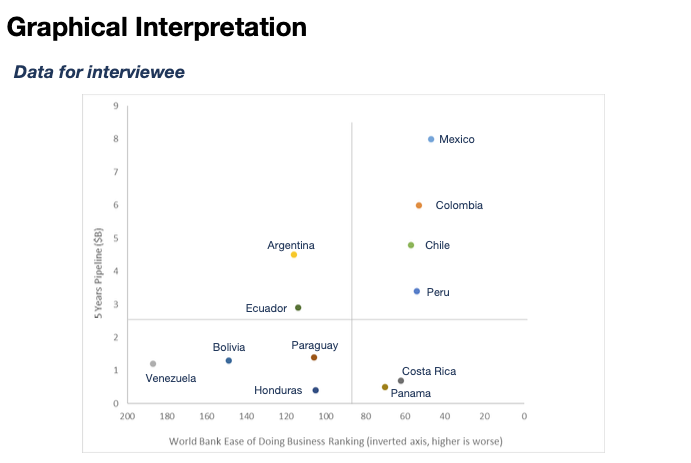

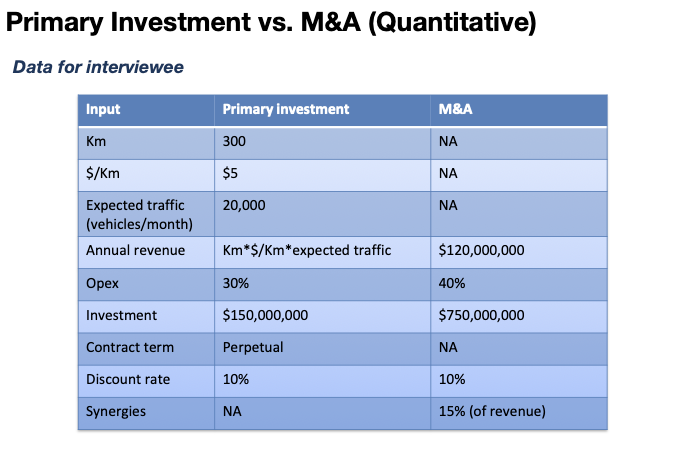

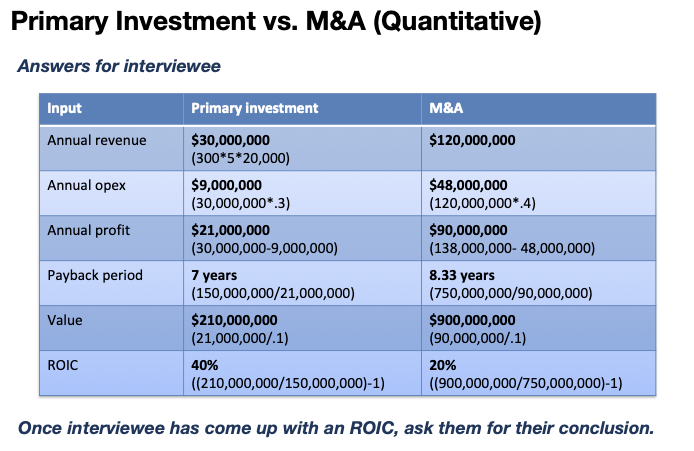

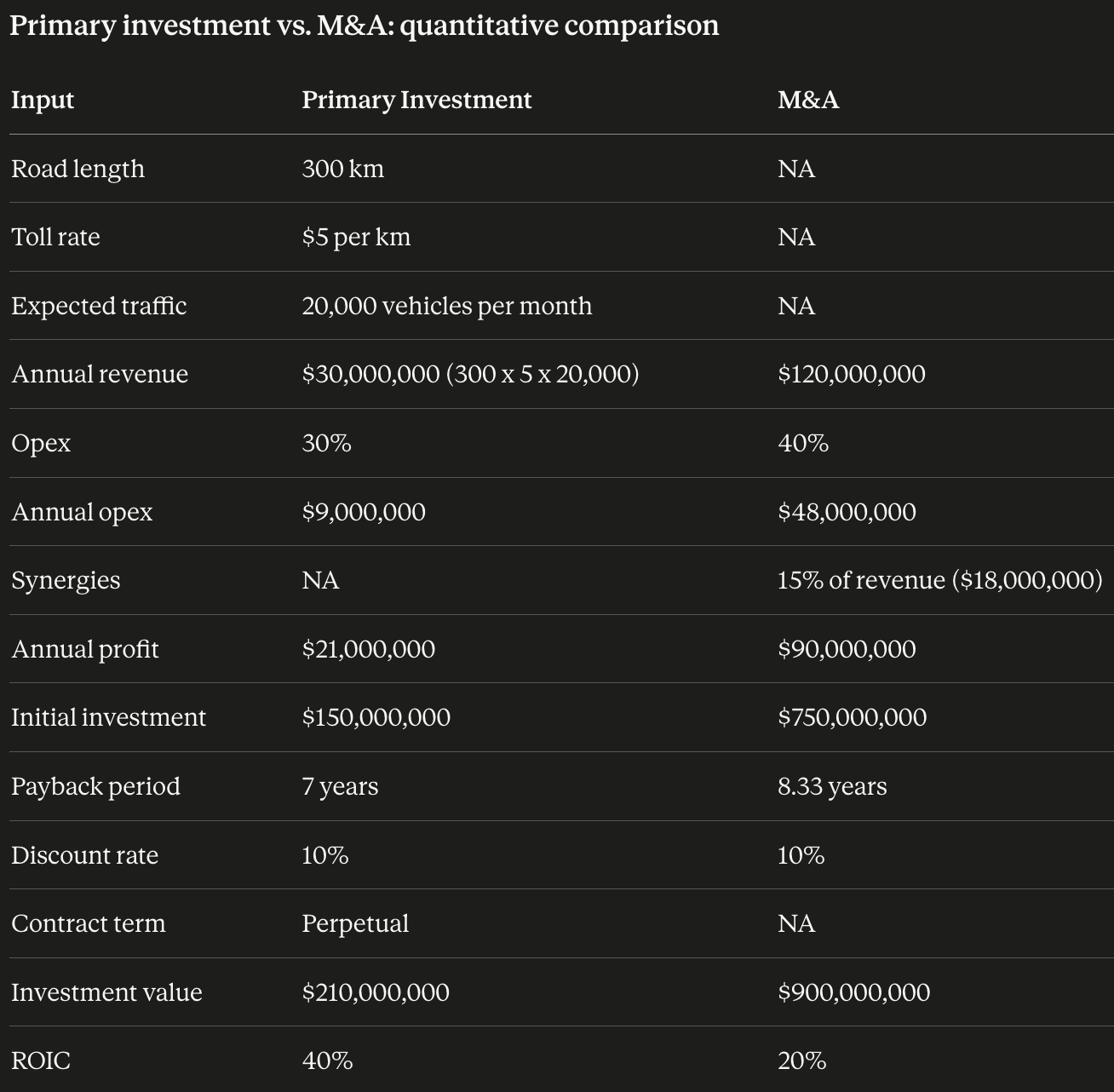

This case has three distinct phases, each of which builds on the previous one. The qualitative framework sets up the market selection, the scatter plot narrows the geography, and the ROIC calculation settles the entry mode question. Phase 1: Framework for international expansion The four dimensions to cover are culture and management complexity, political environment, pipeline and economic prospects, and competitive environment. The insight that matters most at this stage is that the client's Portuguese-speaking, Brazil-based management team is going to find South American markets far easier to operate in than, say, Europe or Asia. Cultural proximity and language are meaningful competitive advantages in a business that requires long-term government relationships. This is the primary justification for limiting the geographic scope to South America. Phase 2: Market selection from the scatter plot Read the axes carefully before drawing conclusions. The x-axis is inverted, which is a deliberate test of graphical literacy. Countries to the right are easier to do business in, not harder. Once that is understood, the upper right quadrant clearly contains the preferred targets: Mexico, Colombia, Chile, and Peru. These four offer the combination of a large near-term pipeline and a business-friendly environment. The case instructs that Costa Rica and Panama can be noted but have limited pipeline. Argentina is a judgment call: its pipeline is real but the operating environment is more challenging and the country has a history of regulatory instability. Phase 3: Primary investment vs. M&A Before receiving the data, the candidate should be able to state the inputs they would need: for primary investment, road length, toll rate, expected traffic volume, opex rate, initial investment, contract term, and discount rate. For M&A, revenue, opex rate, synergies, initial investment, and discount rate. Once the data is shared, the calculations are not technically difficult but require careful organisation: Primary investment annual revenue: 300 km x $5 per km x 20,000 vehicles per month x 12 months = $36M. Wait, note that the answer sheet shows $30M using vehicles per month without annualising separately, implying the $5 per km toll is an annual figure. The case answer confirms $30M, so accept that as given. The ROIC comparison tells a clear story: primary investment generates a 40% return on capital while the M&A route generates 20%. The payback period is also slightly shorter for primary investment at 7 years versus 8.3 years. Even though the M&A generates more absolute profit, the price paid is too high relative to the value created. Final recommendation: The client should enter one of the shortlisted South American markets — preferably Mexico, Chile, or Colombia given their combination of pipeline size and business environment quality — through a primary investment rather than an acquisition. The ROIC on primary investment is double that of the M&A route at 40% versus 20%, and the payback is shorter. Cultural and linguistic proximity to Brazil supports the South America focus. Follow-on steps worth flagging: assess whether further price negotiation on the M&A target could change the ROIC calculation enough to reconsider; run sensitivity analyses on traffic volume assumptions and macroeconomic factors, since concession revenues are highly exposed to GDP and vehicle growth rates; and assess the likelihood of winning competitive RFPs in the target country as a new entrant, since being a foreign operator bidding against established local players is a real execution risk.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".