Car Wash Chemical Company

Practice with AI

Hone your skills by practicing this case with our AI-powered consultant.

Walter Black Industries Inc. is a privately owned chemical manufacturing company specializing in car wash chemicals. The client wants to grow revenues by 30% without sacrificing profit margins. This is a growth strategy case that tests your ability to systematically identify revenue levers — across pricing, volume, product mix, and new channels — while protecting margin integrity.

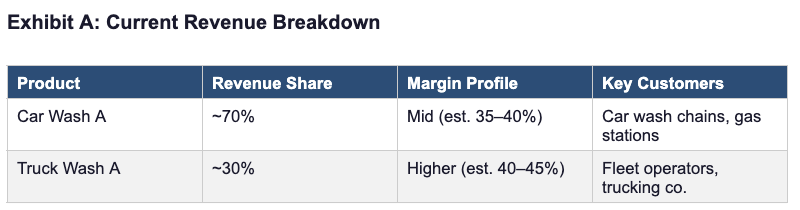

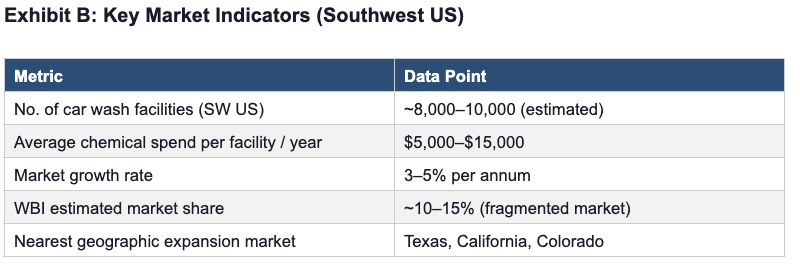

Walter Black Industries Inc. (WBI) is a privately owned chemical manufacturing company based in Albuquerque, New Mexico, United States. The company specializes in producing car wash chemicals and has been in operation for over 15 years. The company has two major product lines: Car Wash A — a chemical solution used in automated and self-service car wash operations Truck Wash A — a heavy-duty variant designed for commercial truck and fleet washing WBI sells its products primarily to car wash operators (B2B), including standalone car wash facilities, gas station car washes, and commercial fleet operators. The company has an established customer base in the Southwest United States but has not meaningfully expanded its geographic footprint or product portfolio in recent years. The client has recently brought in a new CEO who has set an ambitious growth target. WBI has hired your consulting firm to identify actionable opportunities to achieve this goal.

The client has hired our consulting firm and would like us to identify opportunities for growth. Their goal is to increase revenues by 30% without reducing profit margins. How would you go about it?

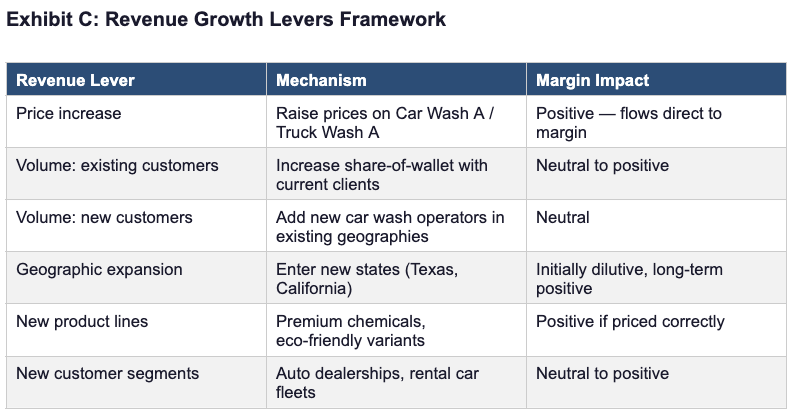

Suggested Case Structure Open with a revenue decomposition framework: Revenue = Price × Volume | Volume = # Customers × Units Per Customer Break down the 30% revenue increase into component levers, then prioritize by: (1) speed to impact, (2) margin neutrality or improvement, (3) execution feasibility. Priority Recommendations 1. Pricing optimization (Quick Win): Analyze price elasticity across the customer base. Even a 5–10% price increase on Car Wash A — if retention holds above 85% — contributes meaningfully to the 30% target with no margin dilution. 2. Increase share-of-wallet with existing customers (Medium-term): Introduce bundled offerings (Car Wash A + ancillary products), annual supply contracts, or loyalty discounts for volume. Cross-sell Truck Wash A to car wash operators who manage fleet vehicles. 3. Geographic expansion — Texas as beachhead market (Medium-term): Texas has a dense car wash market and is adjacent to WBI's existing Southwest footprint. A targeted sales push into Texas, leveraging the existing product portfolio and supply chain, can add meaningful volume without requiring new product development. 4. New customer segments — auto dealerships and rental fleets (Longer-term): These segments have higher average order values and longer contract cycles. Penetrating even 2–3 regional fleet operators could materially move the revenue needle. Requires a separate B2B sales motion and potentially custom product formulations. Quantitative Sanity Check If current revenues = $10M (hypothetical), WBI needs to add $3M to hit the target. Pricing lever: 8% price increase × $10M base × 90% retention = ~$720K Volume lever (existing market): 15% more customers × $10M base = ~$1.5M New geographies: Texas entry at conservative 5% market share of $5M addressable = ~$250K Y1 New segments: 3 fleet contracts at $200K each = ~$600K Combined, these four levers yield ~$3.07M — sufficient to meet the 30% target while preserving or improving margins.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".

Case Materials

Submissions (0)

Be the first to comment on this case.

Practice with AI

Sharpen your skills by practicing this case with our AI-powered consultant.

Practice Sessions

Note: Accepted practice sessions will be available in your profile under "My Practice Sessions".